Executive Summary

Every net zero target assumes a future world that does not yet exist. Setting such a target is a commitment to help build that world.

Corporate net zero is not a target in the ordinary sense. It is a vision with a target component, and an obligation to act to make the vision possible, even when those actions don't show up in the GHG inventory.

Net zero targets currently bundle two fundamentally different things: emissions a company can reduce through its own decisions, with emissions that depend on policy, technology, infrastructure, or markets changing around them. Treating these the same sets companies up for failure on the parts they can't control, and holds them to account too little on the parts they can.

The bundling also obscures the actions that companies should take to build the world their target assumes, but can’t account for. Many companies tend to focus on actions which fit within their GHG inventories, even when other actions, such as lobbying, market building, innovation support, funding new technologies and non profit organisations can matter more for the climate than anything that shows up in their accounting..

This paper sets out to split net zero into two parts. Mirroring the Paris Agreement's split between unconditional and conditional nationally determined contributions, we separate the part of a corporate net zero target which can be reached under existing policies and markets (the unconditional part) from the part that would require new policy, technology, or system change (the conditional part).

For the first, unconditional part, companies should set ambitious near-term targets and take actions that are visible in their GHG emissions inventory. For the second conditional part companies should spell out what change their net zero targets are conditional on and work to help resolve these conditions, regardless if those actions can count in their emissions inventories or not.

The difference between conditional and unconditional emission reductions does not neatly fit onto GHG Scopes. Many emission sources within Scope 3 can lie within corporate control, and emissions in Scope 1 outside of control due to affordability. Where emissions end up will differ a lot between sectors.

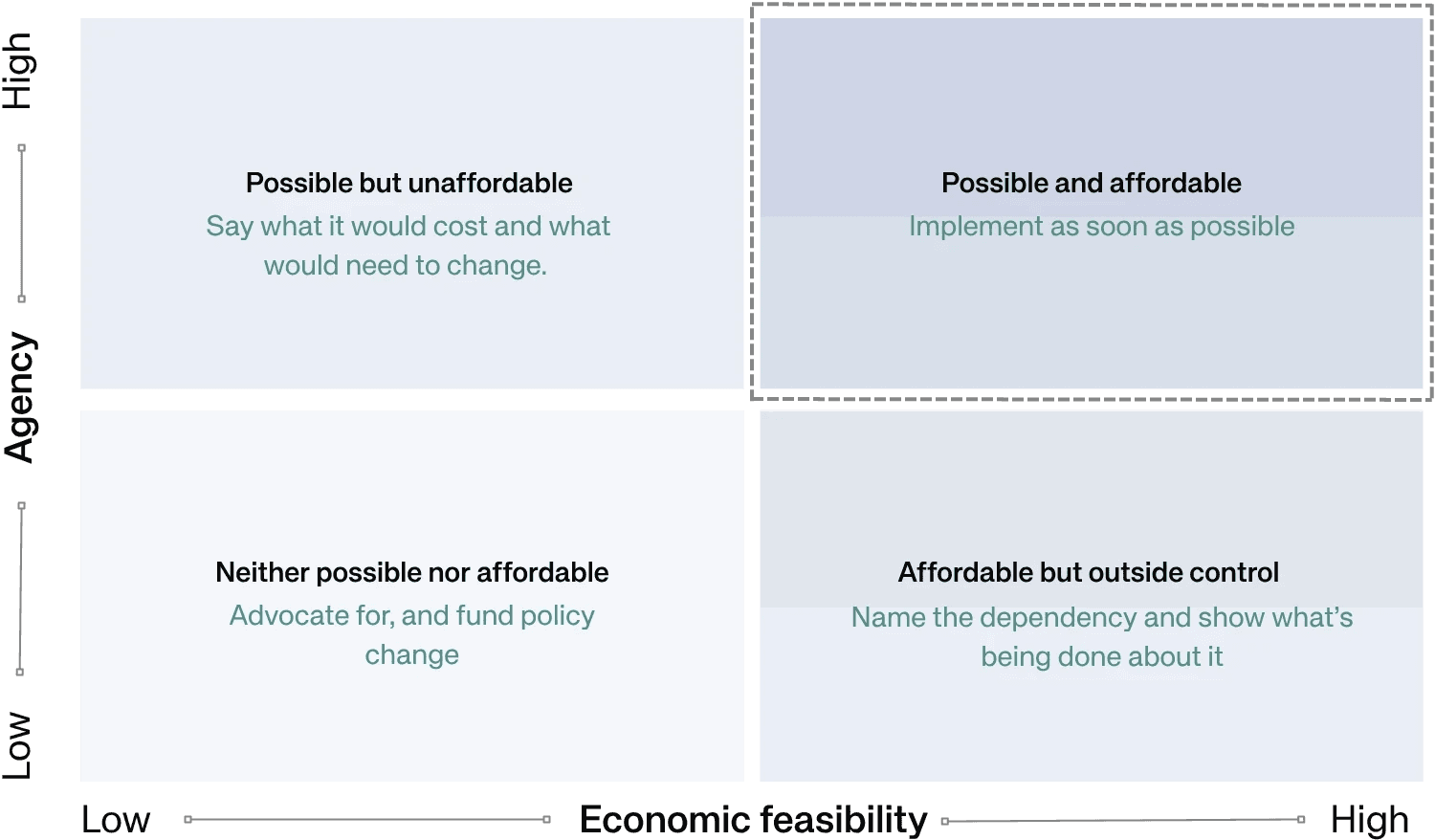

To determine which emissions fit in what part we introduce two factors: corporate agency (can the company directly influence the emission?), and economic feasibility (can it absorb the cost?). Bringing the two together yields a matrix of four quadrants, each with a different obligation:

Possible and affordable — This quadrant is where unconditional emission reductions live. Companies take action to implement changes now.

The three other quadrants constitute the conditional parts:

Possible but unaffordable — here companies should make the cost gap visible and advocate for the policy that closes it.

Affordable but outside control — companies should use commercial leverage and coordinate across the value chain.

Neither possible nor affordable — companies should fund and advocate for the system change on which the target depends.

Declaring emissions conditional does not reduce responsibility. It increases the obligation to fund and push for the policies and solutions that resolve those conditions. A company that classifies most of its emissions as conditional but does nothing to change those conditions is not doing credible climate work.

This concept is not a new standard, reporting format, or governance proposal. It is a diagnostic tool and accountability overlay that companies, investors, and standard-setters can apply alongside existing frameworks. This includes SBTi, ISO’s upcoming net zero standard, and the GHG Protocol, as well as frameworks like the ACT Initiative's transition plan assessments, Oxford Net Zero's Spheres of Influence, the Exponential Roadmap Initiative's Business Playbook, and Mirova and Sweep's Climate Contribution Framework.

It complements these by adding a structured way to distinguish what a company can deliver from what depends on external change, and by creating a logic for determining when financing climate solutions and policy advocacy become obligations rather than optional extras. Trackers like Influence Map make the credibility, or otherwise, of climate action visible by assessing whether a company’s lobbying supports or hinders the transformations on which its targets depend.

This paper explains how the concept of conditional targets can be used in practice, giving concrete guidance as well as examples of how it could fit different sectors. We hope that this concept contributes to increasing the ambition of net zero targets, to becoming more honest about constraints, and to turning advocacy from optional positioning into a measurable obligation in proportion to dependency.

Introduction

Imagine an automobile company that has set a target of zero deaths in their cars. It would be obvious to all that the fulfillment of that target to a large extent lies outside of the company’s control. They can make their cars safer, introduce automatic systems, better airbags and compression zones. But to meet their target, society would need to build safer roads, lower speed limits and stricter enforcement of traffic laws. This would not be a target in the normal sense of the word, where targets are SMART: specific, measurable, achievable, relevant, and time-bound, instead we would view it as a vision. To have a credible vision however, the company would not only need to work on their own cars, but also push for the broader changes needed for their vision to be achieved. Corporate net zero works the same way: it is a vision with a target component and an obligation to act to make the vision possible.

In January 2026, Milkywire published A New Lens on Net Zero which introduced the concept of conditional corporate net zero targets. This is a concept for clarifying which parts of net zero targets companies can reach with their own actions under existing climate policies (the unconditional part), and what new policies and solutions would be needed for them to reach net zero (the conditional part).

This mirrors the practice under the Paris Agreement¹, where countries set unconditional Nationally Determined Contributions, which they commit to achieving on their own, and conditional more ambitious contributions that can be achieved with the help of outside support.

The purpose of applying this concept is to clarify the changes needed to reach net zero, what we can expect from corporate action and what other changes are needed. The concept makes corporate net zero more transparent and credible, and sends a clear signal to policymakers and the broader society of what changes are needed. At the same time, the unconditional component identifies which emission reductions companies can achieve under current policies, making it easier to hold them accountable for their promised actions.

Today's corporate net zero targets are already de facto conditional². This is, however, rarely made explicit, which leads to a false sense of target achievability, less pressure for policy change and too limited a view of what companies should be doing.

Importantly, declaring emissions reductions conditional should not mean reducing effort or lowering responsibility. Instead it should increase a company's obligation to fund and push for the policies and solutions that resolve those conditions.

¹ The conditional/unconditional split for national pledges originated in NAMAs under the Cancun Agreements (Decision 1/CP.16, 2010) and was carried forward into INDC and NDC practice. The Paris Agreement text itself does not use this terminology. Article 4.5 of the Paris Agreement acknowledges that enhanced support to developing countries enables higher ambition, which is the principle underlying the practice. See Pauw, Castro, Pickering and Bhasin (2019), 'Conditional nationally determined contributions in the Paris Agreement: foothold for equity or Achilles heel?', Climate Policy 20(4): 468-484

² If a net zero target contains conditional emissions reductions, then by definition, net zero target fulfillment itself is also conditional.

Figure 1. Corporate net zero as a vision with target components and conditional components. The target components cover what a company commits to deliver. The conditional components cover what a company is accountable for helping make possible. Within the target component, deliverables can be denominated either in tonnes of CO2 (the traditional inventory measure) or in sectoral alignment metrics (see Section 7).

What we are outlining here is not a new standard, reporting framework or governance proposal. Rather, it is a mental model and tool for interpreting and more precisely defining corporate net-zero targets in light of real-world constraints, which could be used by existing and future target-setting and accountability frameworks.

Having articulated the diagnosis, the harder question is implementation. How could the concept be used in practice? And what would the potential implications be? These are the questions this paper sets out to explore.

Is net zero the right target?

If net zero targets are inherently conditional, it’s reasonable to ask whether they even are the right type of target. A further complication is that current Scope 3 accounting often relies on spend-based estimates that do not identify the physical emission sources to which corporate responsibility is being assigned. Several actors have questioned if firm-level targets are the right structure in the first place (see Section 7). But thousands of companies have already set net zero targets, entire standards and accountability frameworks have been built around them, and they remain the clearest available expression of long-term climate ambition.

Abandoning net zero targets would mean starting over with less momentum and less infrastructure. More importantly, scrapping corporate net zero would remove a very powerful mechanism for corporate accountability. Just saying that 'companies should help transform energy and industrial systems' doesn’t create accountability, but ‘your net zero target depends on those systems changing, so you are obligated to help build them' does. We argue that net zero target ambitions can be a hook which keeps companies invested in the overall system transformation.

The more productive question now is how to make net zero targets more meaningful by turning aspirational commitments into effective strategies that distinguish between what companies can deliver on their own and what depends on the world around them changing. That is what this framework attempts to do.

What is conditional?

Is it possible to define which emissions reductions are within corporate control versus the reductions conditional on external change? Not precisely, but precision is not needed for the concept's usefulness. To which degree emissions reductions are conditional will always be somewhat subjective and differ widely between companies and business models. But in our view a rough distinction between conditional and unconditional reductions is more useful than one precise-looking target that conceals major dependencies outside corporate control.

As set out above, this split is an allocation rule: it determines which kind of accountability applies, not whether accountability applies at all.

Corporate net zero is constrained by agency and economic feasibility

Whether a company can deliver on an emissions reduction target depends on two main factors.

The first is corporate agency: can company action control an emission source ? Put simply, it's the degree to which a company can make specific reductions happen, regardless of money. Even when a solution is cheaper than the alternative, or the company can afford the green premium, implementing it may lie outside of their control.

Many emission reductions lie within corporate agency e.g. they can shift their own vehicle fleets to electric, order clean transportation, buy green construction material for buildings that they construct. And then they can, in many cases, assist tier 1 suppliers to switch to fossil-free energy.

But other emissions remain outside corporate agency. For example, in many product categories, companies cannot simply purchase a low-emission version of the product today. Instead, their emissions are conditional on suppliers decarbonizing production and supply chains, especially where supply chains are long and complex. Smartphones are one example. A company can buy from a supplier with stronger climate commitments, but it cannot currently buy a genuinely low-emission smartphone in the same way that it can buy low-carbon steel or durable carbon removal. Its Scope 3 smartphone emissions therefore depend largely on whether manufacturers reduce emissions upstream. Similarly, it's not possible for companies to reduce the emissions intensity of electricity used in sold products.

The second factor is economic feasibility: Some solutions are not economically feasible for some companies today, even if the emissions are in their control. Examples include installing carbon capture and storage for heavy industry, which depends on carbon pricing policies to level the playing field. Feasibility is company- and policy-regime specific. What's feasible depends on sector margins, how competitive the market is, and what regulatory framework companies are operating in. That's why there's no universal threshold for what counts as "affordable." But being explicit about where the line is drawn, enables others to check the justification.

Economic feasibility is not binary but comes in degrees. Some companies may be willing and able to take profit cuts to afford projects that reduce emissions, especially non-publicly listed companies that don't have to answer to shareholders. But at the extreme, actions that cost more than a company's entire profit are wholly unfeasible. But in general there is no sharp cut-off where an action goes from being feasible to unfeasible.

Demand for lower-carbon products can change what is affordable for suppliers. For example, if customers are willing to pay a premium for green steel, the steel producer may be able to invest in lower-emission production while maintaining profitability, at least if they are a first mover. Without that demand, the same investment may be technically possible but commercially unrealistic. But, in general, demand for low carbon products tends to require policy support to scale. For example clean demand policies like the EU's vehicle standards, which mandate ever decreasing emissions from new vehicles sold.

Conditionality is not static. What counts as conditional changes over time as policy, technology, and markets evolve. Deploying solar power was conditional on subsidies for many in 2010, but today solar power is unconditional nearly everywhere, and electric vehicles have a similar story. So the conditional portion of companies’ emissions reductions targets should decrease over time. A company that still considers the same parts of its GHG emissions reduction targets conditional in 2035 as it did in 2025, despite significant climate-friendly policy and technology shifts in between, is likely not keeping up. Conditionality should shrink as the world moves.

Using the concept in practice

How would a company work with this concept? Companies would look at each emission source in their inventory and see where it fits on the agency and feasibility matrix. That means listing options for reductions and identifying which ones they have agency over and which of those are economically feasible. The best place for this disclosure is likely in corporate transition plans. The actions to follow depend on where on the matrix the emissions reduction falls. Each quadrant maps to a different type of worldbuilding action. The four sections below describe what action is required in each quadrant, and the position-specific variations within it.

Figure 2: Emissions sit anywhere on the agency and feasibility axes. The four quadrants are heuristic groupings for discussion; Position on the matrix identifies the worldbuilding action required: implement, fund the cost gap, engage suppliers, or advocate and finance system change.

Possible and affordable (upper right quadrant):

Action: Implement as soon as possible.

These are things like electrifying vehicle fleets, buying green construction materials, ordering clean transport. This is the unconditional part of the corporate target. Companies that have not yet acted on these emission sources should explain why not publicly. Knowing that these explanations will be public would accelerate internal decision-making.

Position on the agency axis varies even within this quadrant. At the top sit emissions under the company's direct operational control. Electrifying fleets, sourcing renewable electricity for owned facilities, decarbonising offices. Closer to the threshold, but still in the 'possible' half, sit tier 1 supplier emissions where the company drives change through procurement decisions and supplier engagement.

Affordable but outside control (lower right quadrant): Action: Name the dependency and show what’s being done about it.

Companies would name these emission sources, explain why they are outside of their control and what change reductions depend on, and then show what they're doing to address these emissions, e.g. supplier engagement, providing supplier financing, running coordinated policy advocacy aimed at the specific blocker. Supply chain collaboration is central to this quadrant. The most credible companies here are the ones coordinating action across their value chain, not just asking suppliers to report emissions.

Position on the agency axis matters here too. Emissions just below the agency threshold are likely to cross into the possible-and-affordable quadrant within a few years as solutions mature. For example electrified trucking may be unavailable to purchase for all transports today, but may be possible within a few years. Emissions deeper down in the quadrant, further from the threshold, are likely to stay outside corporate control in the medium to long-term, for example electricity-related emissions from use of sold products.

Possible but unaffordable (upper left quadrant):

Action: Say what it would cost and what would need to change.

This is where heavy industry often sits. A steel producer may control its own blast furnace, but switching to green hydrogen or installing CCS without a carbon price high enough to level the competitive playing field would destroy margins. Here companies should make the cost gap visible: show the green premium they need to charge, what the carbon price would need to be, or what subsidies or contracts for difference would close the gap.

They should also report their actions to push for those policy changes. For example, a company whose target depends on carbon pricing should be advocating for carbon pricing. This is where advocacy credibility matter most. A company whose targets depend on policy change but whose lobbying, or whose trade associations' lobbying, opposes that change does not have a credible target. Organizations like Influence Map already track the alignment between corporate climate commitments and real-world lobbying, and this kind of scrutiny will likely increase.

Neither possible nor affordable (lower left quadrant): Action: Advocate for, and fund policy change if a company has neither agency to reduce the emissions nor can afford to, that's the fully conditional part.

These are emissions for which the company's role shifts entirely to advocacy, coalition-building, and funding. Examples include emissions deep in a supply chain (third to nth tier) suppliers in countries without climate policy), use of sold products on dirty grids, employee commuting, materials that don't yet exist in clean versions. The company can't reduce these emissions through its own actions and couldn't absorb the cost of changing the entire value chain. What it can do is fund and support enabling work that would make reductions possible, such as supporting policy reform in key markets, investing in early-stage technologies, and joining industry coalitions pushing for sector-wide change.

Typical emissions categories that have a large share of conditional emissions for almost all companies:

Use of sold products for electric appliances

Raw materials (significant for the mining industry for example)

Employee commuting

Deep supply chains, second to nth tier suppliers

Investments (especially if Scope 3 emissions of investees are counted)

Companies already have target structures: SBTi near-term targets (typically 5-10 year horizons), long-term net zero commitments and, increasingly, transition plans. Conditional targets are a diagnostic overlay on these existing structures. In practice, the unconditional part of a company's target should roughly correspond to what a credible near-term SBTi target covers: emissions over which the company has agency and for which it’s economically feasible to act within the target period. The conditional part maps to the longer-term, system-dependent reductions that companies commit to but can't deliver alone. Section 7 explores these relationships in greater depth.

What this looks like for investors and evaluators

The conditional targets lens gives outsiders a structured way to assess whether a company's climate strategy is credible. An investor could assess portfolio companies by whether they're taking the actions appropriate to their specific emission sources, essentially applying a version of this logic. The conditional targets lens makes that assessment more systematic: for each quadrant, is the company doing what's appropriate I.e. acting on what they control, pushing on what they can influence, funding what they depend on?

To the extent possible, companies should also be transparent about where climate spending goes. Three categories matter most:

Direct operational decarbonisation, which is often embedded in regular capex and harder to isolate.

Supplier engagement and procurement programmes aimed at decarbonising tier 1 and beyond.

Funding for the system change the conditional share depends on, including advocacy spend, R&D for solutions that don't yet exist at scale, durable carbon removal purchases, climate finance, and coalition contributions. The third category is usually identifiable as discrete budgets.

How this plays out sector by sector

Different sectors face distinct barriers to decarbonisation, so a company's conditional targets depend on the industry in which it’s operating.

For high-margin companies with low relative emissions, agency is often the binding constraint. If they have agency, they usually also have economic feasibility. For global actors this means that radical reductions are dependent on the pace of the global transition to clean energy and transport.

For heavy industry, economic feasibility is the largest constraint. They often have agency in theory (control of their own factory for example), but not in practice because margins are thin and competition is brutal, making them dependent on policies like carbon pricing, to level the playing field.

Of course where a specific company, or a specific emissions reduction action fits in this mapping also depends on the relevant policy environment. For example, all other things being equal, it is easier for a European large utility to shift to fossil-free energy than for an American one since the EU ETS price mechanism makes it more affordable compared to the fossil option.

Below are illustrative splits for a few select sectors. These should be treated as indicative and not definitive. The point is to show how the conditional target lens could apply differently across business models.

Heavy industry (e.g. steel, cement): For a steel producer, a subset of emissions can be reduced unconditionally through energy efficiency, increased scrap recycling, and switching a few facilities to green production where demand from first movers already exists. The majority of its emission reductions are however likely to be conditional on sufficiently high carbon pricing (through a carbon tax or emissions trading), strong border adjustment mechanisms to protect against imports, and subsidies like capex grants or contracts for difference to close the cost gap. A steel producer in the EU may be able to reach net zero with today's policy trajectory (if current EU ETS plans hold), while in a country or region without carbon pricing a net zero target would be almost entirely conditional.

High-margin companies (e.g. tech, software, retail of own high-value products): For a large tech company, economic feasibility is rarely the binding constraint and they can afford green premiums. Agency is the limiting factor. They can control their own operations, direct suppliers, and can invest in 100% fossil free energy for data centres and offices. But use of sold products (emissions from customers using their devices on dirty grids), employee commuting, and deep supply chain emissions, which often make up the majority of the company’s emissions, are mostly outside their control. A large limiting factor is grid decarbonization in markets where they sell products.

Supply-chain-heavy sectors (e.g. mining, fashion, food retail): Mining companies can electrify their own equipment and transport (unconditional, relatively small part of total emissions). But for many, the vast majority of their indirect emissions are in Scope 3 Use of Sold Products e.g. the iron ore becomes steel through a very emission intensive process. Reducing those emissions is conditional on their customers decarbonizing, which in turn depends on policy and market transformation. Food retailers are similar. They can switch to green energy in their stores, electrify their own transports, and promote greener alternatives in stores. But they stock tens of thousands of individual products from thousands of suppliers and their scope 3 emissions rely on economywide decarbonization and behaviour change.

Applicability beyond companies

This paper focuses on companies, but the basic logic applies more broadly.

Countries. Low-income countries already use conditional targets splitting their Nationally Determined Contributions into an unconditional part (what they'll do with domestic resources) and a conditional part (what they could achieve with international support). The corporate conditional targets concept mirrors this structure.

Countries consumption-based emissions, the emissions caused by all consumption in the country, including imports and travel, is similar to corporate scope 3 emissions. Countries can implement policies for sustainable consumption, but a subset of the imported emissions are conditional on trading partners decarbonizing. This can be somewhat influenced with diplomacy and support for international climate policy.

Individuals are similar to companies. They can choose to fly less, eat less meat, switch to public transport, or buy an electric car. But people can't change the energy grid, the public transport system, or how their apartment building is heated. The share of conditional versus unconditional differs massively between locations. A Swede, who lives in a country with nearly fossil-free electricity generation, has a much larger unconditional share of personal emissions than someone in Poland, where the grid is still largely coal-powered. But they can both vote for parties with ambitious climate policies and advocate for change.

Both these levels deserve deeper analysis, but the underlying logic is the same: separate what you control from what you depend on, act on the first, and push for change on the second.

Challenges and limitations of the concept

There's an obvious risk in using the concept: companies could hide behind conditionality. They could declare most of their emissions conditional to justify inaction. That risk is real, and it's why the concept would require companies to be specific about what they're doing for each bucket - conditional and non-conditional - not just which bucket their emissions fall into. A company that declares 80% of its emissions conditional but does nothing to change the conditions is not doing credible climate work. The conditional/unconditional distinction does not divide emissions by accountability or no-accountability but by which kind of accountability applies. If a company misclassifies an emission as conditional, the consequence is that it is held to worldbuilding action rather than numerical reduction.

Still, some companies could still use conditionality as a cover for doing less. Several safeguards help reduce this risk:

First, transparency: companies applying this framework should publicly disclose which emissions they classify as conditional and which as unconditional, as well as what specific dependencies (policy changes, technology availability, supplier decarbonisation, market conditions) the conditional components rests on, and what actions they are taking to address those dependencies.

Second, peer comparison: if a competitor in the same market and policy environment treats an emission source as unconditional, a company that classifies the same source as conditional needs to explain the difference.

Third, directionality: as described above, the unconditional share should grow over time, and a company whose conditional emissions bucket isn't shrinking needs to explain why.

Fourth, external scrutiny: investors, standard-setters, and civil society can challenge classifications, especially when companies in the same sector diverge significantly. The framework's value depends on this scrutiny.

But more importantly, the alternative to this framework isn't rigorous unconditional net zero target fulfilment, but net zero abandonment. Current corporate net zero risks collapsing under its own weight as companies get closer to the target deadlines and realize they can’t meet them.

The concept can also create the opposite of moral hazard: more pressure for policy change, and more pressure on companies to fund the types of actions that will bring about the systemic changes their targets depend on. Whether the use of the concept tips toward excuse-making or increased accountability depends on how rigorously it's operationalised.

Defining where the line falls between conditional and unconditional won't be precise. That's acceptable. The value lies in the conversation it prompts, giving nuance to current ways of assessing the ambition and credibility of companies’ targets. Right now, companies are evaluated as if all their emissions are equally controllable. Progress towards a net zero target is assessed on a single metric (total annual emissions) , when in reality some of that progress depends entirely on the company and some depends on the world around them.

Relationship to existing frameworks and standards

The conditional targets concept doesn't exist in a vacuum. Several frameworks already address parts of what we describe here, and emerging standards are moving in a compatible direction.

Existing frameworks

The ACT Initiative (Assessing Low Carbon Transition), hosted by the World Benchmarking Alliance and originally developed by ADEME and CDP, is the most comprehensive framework for assessing the credibility of corporate transition plans. It evaluates companies against sector-specific low-carbon trajectories across governance, targets, strategy, and financial planning. Conditional targets complement ACT by providing a structured way to distinguish between what a company can deliver within its transition plan and what depends on external change.

Oxford Net Zero's Spheres of Influence highlights that companies have different capabilities for helping achieve global net zero, beyond their own GHG reductions. It defines three spheres of corporate agency: Products and Services (scaling climate solutions), Portfolio of Climate Finance (financing climate action), and Policy and Public Engagement (advocating for climate solutions). The conditional targets framework creates a direct logic for when these spheres become obligations rather than optional extras: if your net zero target depends on conditions you can't deliver, then financing climate solutions (Sphere B) and advocating for enabling policy (Sphere C) are requirements, not nice-to-haves.

Influence Map tracks whether corporate lobbying aligns with stated climate commitments. They assess whether companies fulfill what they promise when setting conditional targets. For example, if a company's target depends on carbon pricing but their trade association lobbies against it, they have failed the most basic credibility test.

Mirova and Sweep's Climate Contribution Framework evaluates corporate climate action across three levers: carbon footprint reduction, deployment of climate solutions, and climate finance. Their framework takes the different capabilities of companies into account and gives scores both for possible potential and realized potential This is an example of how companies’ ambition and progress can be assessed by third parties while taking their different capabilities into account.

The Exponential Roadmap Initiative's (ERI) Business Playbook lays out five pillars of corporate climate action: cut operational emissions, decarbonize value chains, build and scale climate solutions, mobilize finance, and shape policy and narrative. The conditional targets concept connects naturally to this structure. The unconditional share of a target maps primarily to Pillars 1 and 2. The conditional share creates obligations under Pillars 3, 4, and 5, making Pillar 5 (shape policy) not optional but a direct consequence of having conditional emissions.

New Climate Institute's work on Corporate Climate Responsibility argues that Scope 3 accounting is too flawed to support corporate net zero targets, and proposes transition-specific alignment targets (TSATs) as a complementary or alternative measurement layer: sector-specific indicators such as share of zero-emission vehicles sold, share of near-zero-emission materials procured, or share of cloud workloads on 24/7 carbon-free energy. Conditional targets share the diagnosis that treating all corporate emissions as equally deliverable does not work, but keeps the net zero target frame and makes it more honest about dependencies. We see the two approaches are highly complementary.

Michael Gillenwater at the Greenhouse Gas Management Institute, with Derik Broekhoff at the Stockholm Environment Institute, has proposed a different multi-statement GHG reporting framework where the emissions inventory only consists of emissions based on physical data, not spend data and emissions factors. Much of current Scope 3 data would be excluded. They also propose a separate Mitigation Intervention statement that uses consequential accounting to recognise beyond-inventory actions on their own terms; non-GHG transition indicators where they apply; and a residual Value Chain Analysis that replaces today's Scope 3 as a hotspot-identification tool rather than an accountability metric. This approach largely abandons corporate net zero as defined today. We share their diagnosis, but our proposal preserves net zero as an overarching ambition that motivates companies to engage in the worldbuilding actions net zero would require.

Lisa Sachs and colleagues at the Columbia Center on Sustainable Investment have a similar diagnosis as this paper, arguing that most impact a company can have lies outside their GHG inventory. They argue that corporate net-zero frameworks “distract from sectoral decarbonization” and propose redefining corporate climate leadership around contributions to systems transformation. This could be interventions such as market creation and system co-design, many of which reduce real-world emissions without showing up in any single firm's ledger. Their idea fits well with the concept this paper lays out with the difference that we are trying to preserve net zero, but reimagine it as a driving force for the transformation.

Standards and protocols

The GHG Protocol is being reworked and the Actions and Market Instruments (AMI) work, out for consultation in early 2026, argues corporate physical inventory cannot capture everything a company does about emissions. AMI's answer is a multi-statement reporting structure. The physical GHG inventory stays as the foundation. Three new statements sit alongside it: a market-based inventory for contractual procurement choices, a GHG impact statement for the consequential effects of actions taken inside and outside the value chain (emissions reduced, avoided, or removed, including financed projects and carbon credits), and a set of non-GHG indicators for things like climate finance contributions and the share of procurement meeting defined criteria. The logic is that attributional and consequential accounting answer different questions and should not be collapsed into one figure.

The SBTi's 2026–2030 Strategy, published in May 2026, as we were preparing this paper for publication, directly acknowledges that most companies cannot reach net zero alone and says the SBTI will put more focus on what companies can influence. Where performance gaps are driven by external barriers, the strategy notes that companies "should engage at the sector or system level". They also clarify that companies making their best efforts but missing their targets can still remain in the SBTi framework and claim they are continuing to progress to net-zero.

The SBTi's Corporate Net-Zero Standard 2.0, soon to be published, moves in the same direction (as per the latest draft). companies act at the level where they actually have leverage: the individual activity, the supplier or customer, a shared "activity pool," or the wider sector. Where aligned goods cannot be sourced because alternatives are location-bound or not yet available at scale, companies can support decarbonization at the sector level instead of being held to a source they cannot change. They also state that transition plans must spell out their key assumptions and external dependencies, and companies are recommended to align their policy engagement and lobbying with their net-zero ambition.

These directions are highly consistent with the diagnosis behind our paper. SBTi stops short of calling targets conditional beforehand, but introduces something like an ex-post conditionality in their new strategy..

We are aware that the forthcoming ISO 14060 standard acknowledges that technical and economic feasibility are relevant for determining what companies can deliver toward net zero. The conditional targets concept is consistent with this direction: it provides a practical way for companies to be transparent about where feasibility constraints limit what they can deliver by the target date, and what they're doing in response.

Market instruments

Standards are currently renegotiating what counts as fulfilling a corporate climate target, particularly around the use of market instruments such as energy attribute certificates and durable carbon removal. This paper deliberately operates one level beneath that debate. It is about the physical emissions a company can eliminate through its own decisions versus those that depend on policy, infrastructure, and markets changing around it, a distinction that holds regardless of how target fulfillment is defined. Importantly, even where instruments are allowed, many companies, especially low-profit, high-emission firms would likely not afford to cover their full inventory with high quality market instruments at any realistic price. For them, the conditional framing is not a stylistic choice but the only honest description of where they stand

What this framework targets adds

Importantly, conditional targets is a diagnostic tool and accountability overlay that companies can apply on top of whatever standard or target setting mechanism they follow. It is meant to complement these frameworks. It uses the existing corporate net zero targets, keeping the ambition, but making the targets more honest, and motivating companies to take further action in support of what would need to happen to make the conditional parts of their targets achievable.

This framework is intended, in part, as a tool for sustainability and climate teams who want to focus their work where it has the greatest impact. Today's corporate sustainability paradigm narrowly rewards action that shows up in the GHG inventory. This can lock companies into prioritising inventory-visible interventions even when other actions could do more for the climate. By making clear which parts of a net zero target depend on system change, and by treating worldbuilding actions as integral to the target rather than separate from it, the framework gives companies a structured way to raise their ambition and direct resources toward the actions that matter most for delivering the world the target assumes.

Where this goes next

Every corporate net zero target rests on an assumed future world that does not yet exist. Setting a target is, implicitly, a commitment to help build that world. The framework proposed here makes that commitment explicit and gives companies, investors, and standard-setters a structured way to assess whether the commitment is being met. It does not ask more of companies than they should be willing to commit to. It asks them to be honest about what they can deliver alone, and to be accountable for the worldbuilding work the rest of their target requires.

Next steps can include corporate testing, applying the concept to specific companies emissions and transition planning. Deeper sector-by-sector analysis of what conditional and unconditional looks like can also be done for specific industries like steel, cement, consumer goods, mining, and fashion. That work will make the concept more concrete and testable. Work can also be done to explore how conditional targets interact with existing standards and reporting frameworks, and how they apply to entities beyond companies.